Student loans loan forgiveness is a crucial topic for millions of borrowers seeking financial relief. If you're one of them, this guide will walk you through everything you need to know. From eligibility criteria to application processes, we'll ensure you're well-informed about your options. Whether you're a recent graduate or a long-time borrower, understanding loan forgiveness programs can significantly impact your financial future.

Student loans have become a financial burden for many individuals across the United States. The rising costs of higher education have left millions of borrowers struggling to repay their debts. As a result, the government and various organizations have introduced loan forgiveness programs to alleviate this burden. These programs aim to provide relief to borrowers who meet specific criteria, making it easier for them to manage their financial obligations.

In this comprehensive article, we'll delve into the intricacies of student loans loan forgiveness, exploring the different programs available, eligibility requirements, and how to apply. By the end of this guide, you'll have a clear understanding of how these programs work and how they can benefit you. Let's get started!

Read also:Bonnieblue Erothots A Comprehensive Guide To Understanding The Phenomenon

Table of Contents

- What is Student Loans Loan Forgiveness?

- Types of Loan Forgiveness Programs

- Eligibility Criteria

- Application Process

- Benefits of Loan Forgiveness

- Common Mistakes to Avoid

- Tax Implications of Loan Forgiveness

- Frequently Asked Questions

- Resources and References

- Conclusion

What is Student Loans Loan Forgiveness?

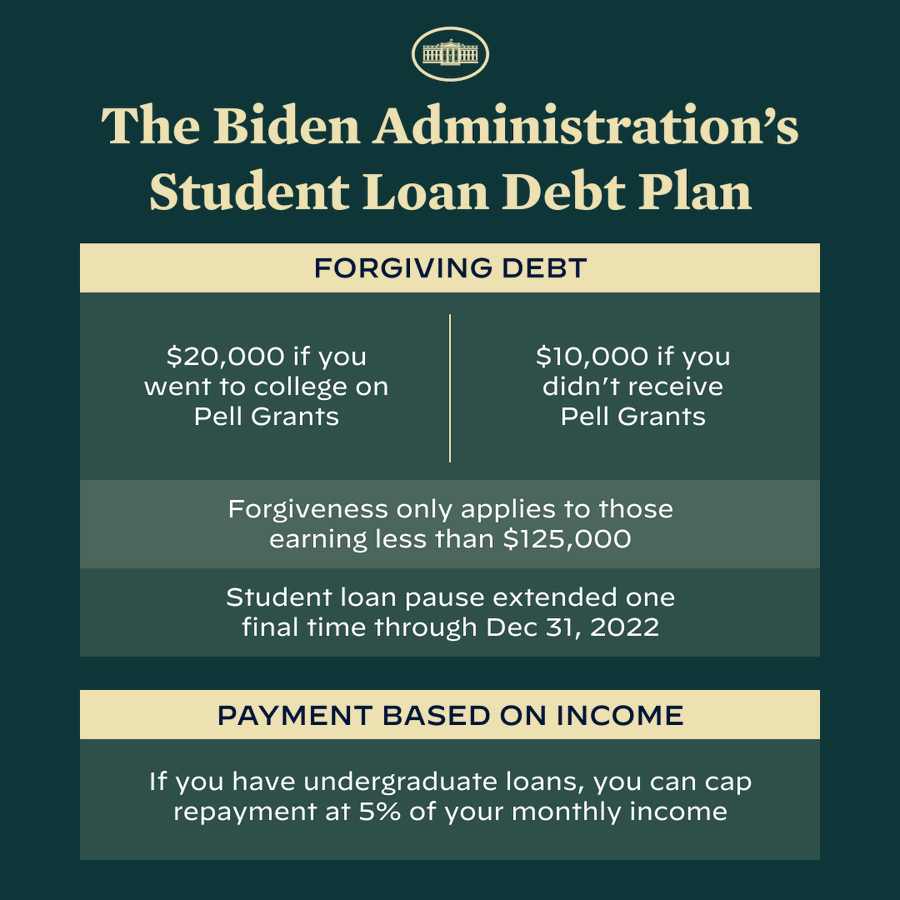

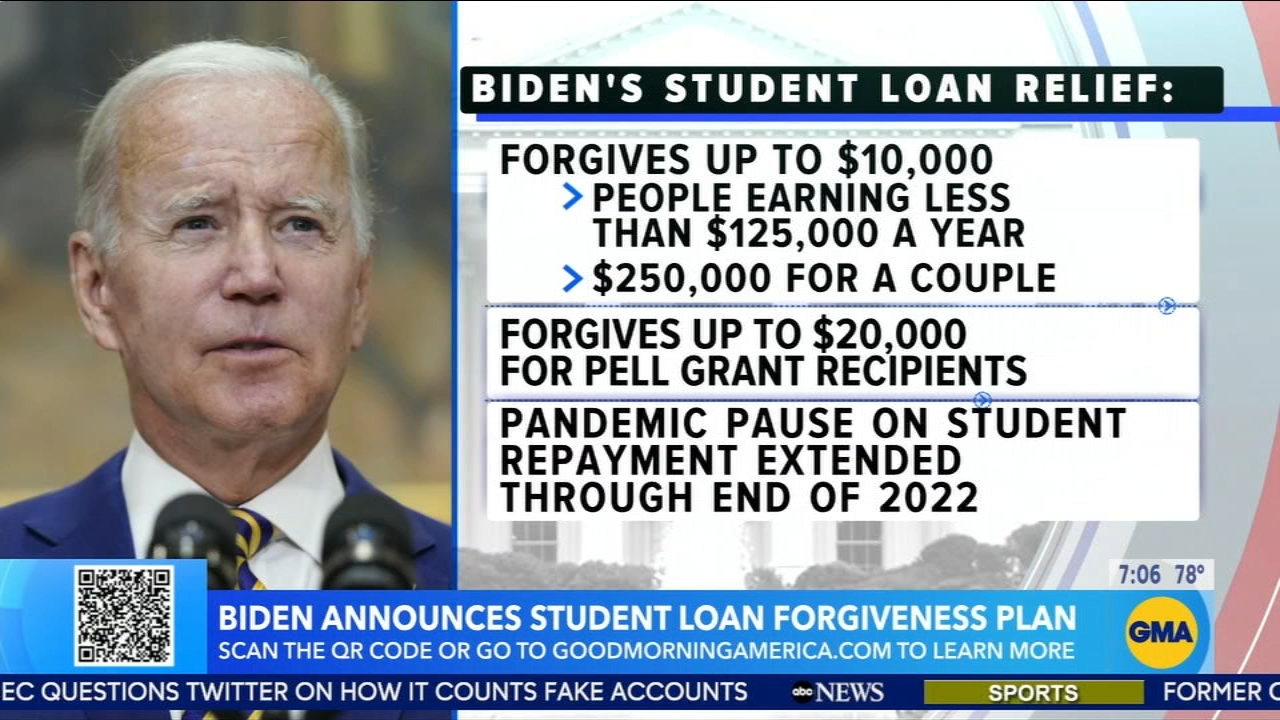

Student loans loan forgiveness refers to programs designed to discharge or cancel a portion or all of a borrower's federal student loans. These programs are typically offered by the federal government and certain private organizations to help borrowers who face financial hardship or work in public service sectors. The primary goal of these programs is to provide relief to borrowers who might otherwise struggle to repay their loans.

Loan forgiveness programs are not a one-size-fits-all solution. They vary in terms of eligibility, benefits, and application processes. Some programs are tailored for specific professions, such as teachers or healthcare workers, while others are available to borrowers in financial distress or those who meet income-based criteria.

Key Features of Loan Forgiveness Programs

- Discharge or cancellation of student loan debt

- Targeted at borrowers with federal student loans

- Varied eligibility requirements based on occupation, income, or financial hardship

- Potential tax implications depending on the program

Types of Loan Forgiveness Programs

There are several types of loan forgiveness programs available to borrowers. Understanding the differences between these programs is essential to determine which one suits your needs best. Below, we explore some of the most common programs:

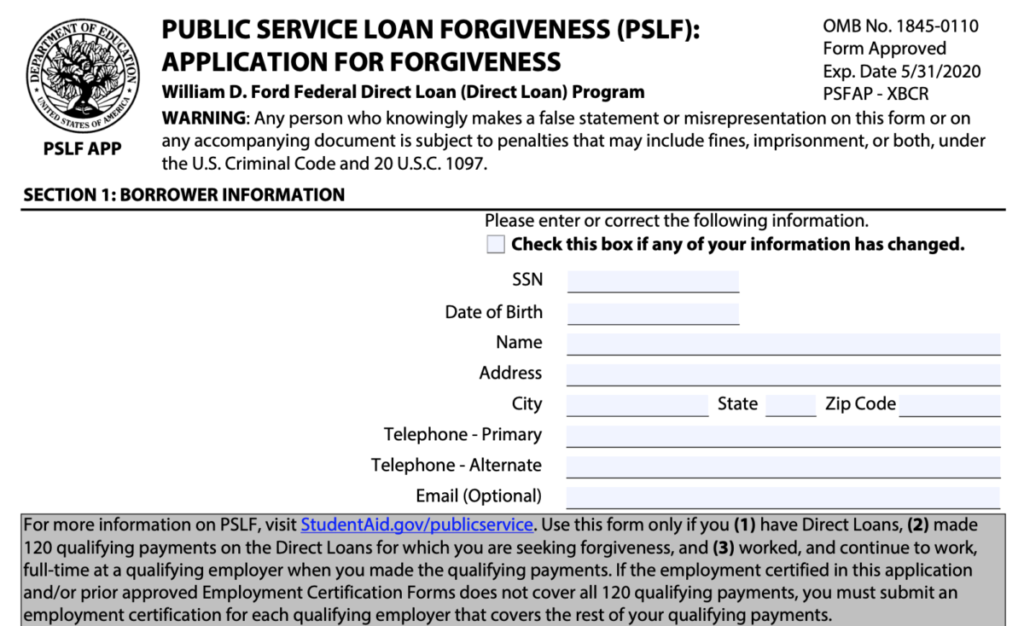

Public Service Loan Forgiveness (PSLF)

PSLF is a program designed for borrowers working in public service jobs, such as government or nonprofit organizations. To qualify, borrowers must make 120 qualifying payments while employed full-time in an eligible position. After meeting these requirements, the remaining balance on their loans is forgiven.

Teacher Loan Forgiveness

This program is specifically for teachers who work in low-income schools or educational service agencies. Eligible teachers can receive up to $17,500 in loan forgiveness after completing five consecutive years of teaching in a qualifying position.

Income-Driven Repayment Forgiveness

Borrowers enrolled in income-driven repayment plans may qualify for loan forgiveness after making a set number of payments, typically 20-25 years, depending on the plan. This option is ideal for those with high debt relative to their income.

Read also:Jeri Caldwell A Comprehensive Look At Her Life Career And Achievements

Eligibility Criteria

Each loan forgiveness program has its own set of eligibility requirements. It's crucial to understand these criteria to determine if you qualify for any of the programs. Below are some common factors considered in the eligibility process:

- Type of loan (federal or private)

- Employment status and industry

- Income level

- Years of service in a qualifying position

For example, PSLF requires borrowers to have Direct Loans and work full-time in a public service job. Borrowers with other types of federal loans may need to consolidate their loans into a Direct Consolidation Loan to qualify.

Application Process

The application process for loan forgiveness programs can be complex and time-consuming. However, following the steps carefully can increase your chances of success. Here's a general outline of the application process:

Step 1: Verify Eligibility

Before applying, ensure you meet the eligibility criteria for the program you're interested in. Review the requirements and gather all necessary documentation to support your application.

Step 2: Submit Required Forms

Each program has specific forms that need to be completed and submitted. For instance, PSLF applicants must submit the Employment Certification Form to verify their qualifying employment.

Step 3: Track Your Progress

Once your application is submitted, it's important to track its progress. Keep records of all correspondence and follow up with the loan servicer if necessary.

Benefits of Loan Forgiveness

Loan forgiveness programs offer several benefits to eligible borrowers. These include:

- Reduced financial burden

- Improved credit score

- Increased financial stability

- Opportunities for career advancement

By taking advantage of these programs, borrowers can focus on other financial goals, such as saving for retirement or purchasing a home.

Common Mistakes to Avoid

While loan forgiveness programs can be highly beneficial, many borrowers make mistakes that can hinder their chances of success. Below are some common mistakes to avoid:

- Not verifying eligibility before applying

- Missing deadlines for form submissions

- Failing to track payments and progress

- Ignoring changes in employment or income

Staying organized and informed throughout the process can help you avoid these pitfalls and increase your chances of success.

Tax Implications of Loan Forgiveness

It's important to note that some loan forgiveness programs may have tax implications. For example, forgiven debt under income-driven repayment plans is generally considered taxable income by the IRS. However, PSLF and Teacher Loan Forgiveness programs are typically tax-free.

How to Prepare for Tax Implications

To prepare for potential tax consequences, consider the following:

- Consult with a tax professional or financial advisor

- Save a portion of your income for potential tax liabilities

- Stay informed about changes in tax laws related to loan forgiveness

Frequently Asked Questions

Q: Can private student loans be forgiven?

A: Private student loans generally do not qualify for federal loan forgiveness programs. However, some private lenders may offer their own forgiveness or hardship programs.

Q: How long does it take to receive loan forgiveness?

A: The timeline varies depending on the program. PSLF, for example, requires 10 years of qualifying payments before forgiveness is granted.

Q: Can I apply for multiple loan forgiveness programs?

A: In most cases, borrowers can only participate in one forgiveness program at a time. However, some programs may allow for overlap or transition between programs.

Resources and References

For more information on student loans loan forgiveness, consider the following resources:

Conclusion

Student loans loan forgiveness programs offer a lifeline to millions of borrowers struggling with debt. By understanding the various programs available, their eligibility criteria, and the application process, you can take steps toward financial relief. Remember to stay informed about potential tax implications and avoid common mistakes to maximize your chances of success.

We encourage you to share this article with others who may benefit from it and explore other resources on our site. If you have questions or need further assistance, feel free to leave a comment or contact us directly. Together, we can work toward a brighter financial future!