The Education Department Has Suspended Some Income-Driven Student Loan Repayment Plans: Here's What Borrowers Should Know

Mar 20 2025

Student loan debt has become a significant financial burden for millions of Americans, and the Education Department's recent decision to suspend certain income-driven repayment plans has sparked widespread concern among borrowers. Understanding the implications of this move is crucial for those navigating their repayment journey. This article will provide a comprehensive overview of the situation, offering guidance and actionable insights for borrowers affected by these changes.

The Education Department's suspension of some income-driven repayment plans has created confusion and uncertainty for many student loan borrowers. With the cost of higher education continuing to rise, more individuals are relying on these repayment options to manage their debt. However, the recent changes mean borrowers need to stay informed and take proactive steps to protect their financial well-being.

This article aims to clarify the details of the suspension, outline the key factors borrowers should consider, and provide practical advice to help manage student loan debt effectively. Whether you're a recent graduate or a long-term borrower, this guide will equip you with the knowledge you need to navigate these challenging times.

Read also:Tom Bradys New Girlfriend A Comprehensive Look At Their Relationship

Table of Contents

- Background on Income-Driven Repayment Plans

- The Recent Suspension: What Happened?

- Which Plans Are Affected?

- Why Was the Suspension Implemented?

- Impact on Borrowers

- Steps Borrowers Should Take

- Exploring Alternative Repayment Options

- Eligibility Criteria for Remaining Plans

- Useful Resources for Borrowers

- Future Outlook and Potential Changes

Background on Income-Driven Repayment Plans

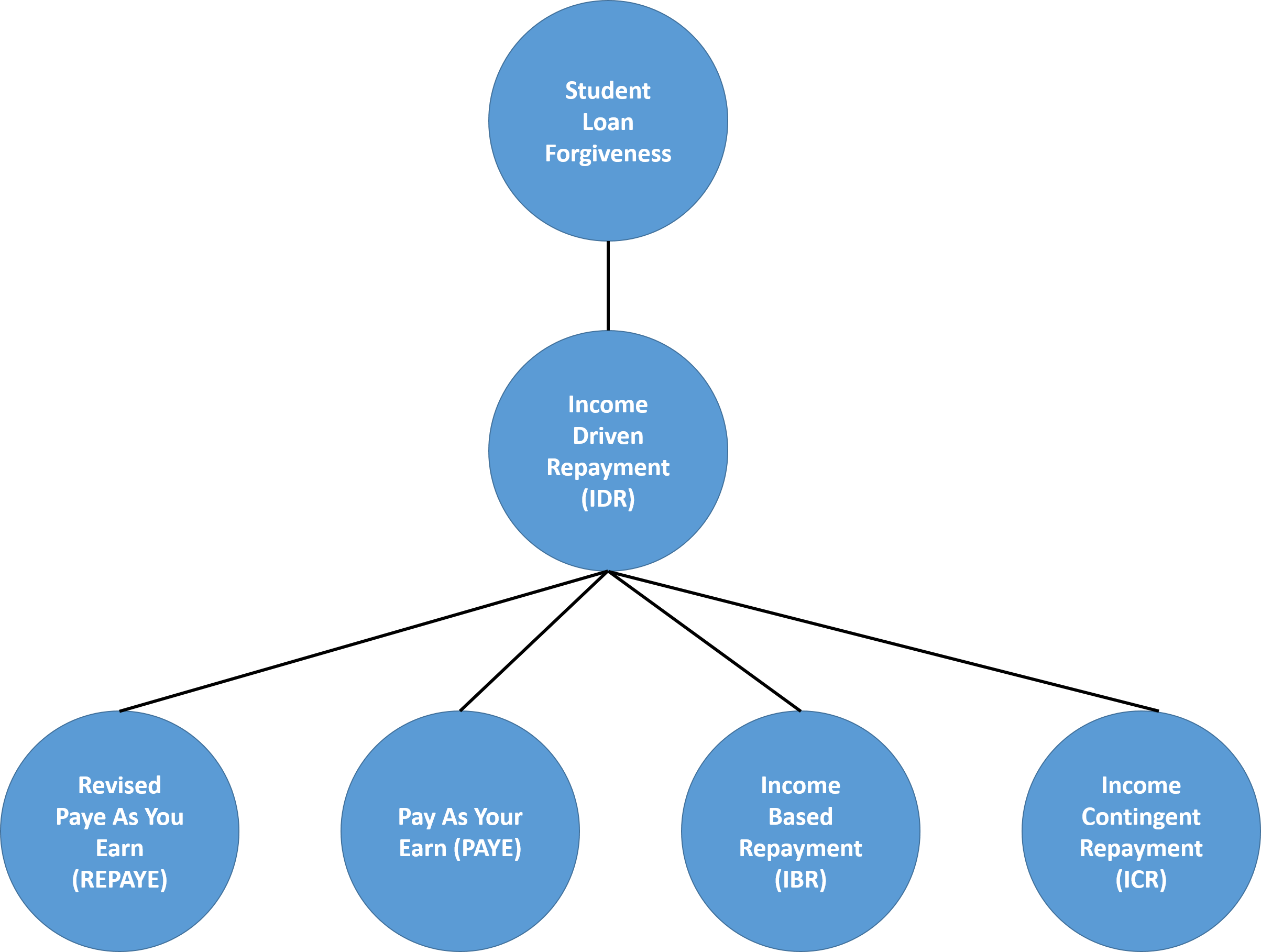

Income-driven repayment (IDR) plans have been a lifeline for many student loan borrowers, offering flexible payment options based on their income and family size. These plans aim to make monthly payments more manageable by capping them at a percentage of the borrower's discretionary income. Some popular IDR plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE).

Under these plans, borrowers typically pay between 10% and 20% of their discretionary income each month. After a set period, usually 20 or 25 years, any remaining balance may be forgiven. However, the recent suspension of certain IDR plans has left many borrowers wondering about their options moving forward.

Key Features of IDR Plans

- Payments are based on income and family size.

- Monthly payments are typically lower than standard repayment plans.

- Eligibility for loan forgiveness after 20 or 25 years.

- Plans are designed to provide financial relief for borrowers with high debt relative to their income.

The Recent Suspension: What Happened?

In a surprising move, the Education Department announced the suspension of certain income-driven repayment plans. This decision was made as part of an effort to review and potentially reform the existing student loan repayment system. While the exact reasons behind the suspension are still being clarified, the department cited concerns about program integrity and fairness.

Borrowers enrolled in the affected plans may face changes to their repayment terms or be required to switch to alternative options. This development underscores the importance of staying informed and understanding the implications of these changes.

Reasons Behind the Suspension

- Concerns about program abuse and misuse.

- Efforts to streamline and improve the repayment process.

- Addressing discrepancies in eligibility criteria.

Which Plans Are Affected?

Not all income-driven repayment plans are impacted by the suspension. The Education Department has specifically targeted certain programs for review, while others remain unaffected. Borrowers enrolled in the following plans may be affected:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

Meanwhile, Revised Pay As You Earn (REPAYE) and Income-Contingent Repayment (ICR) plans are not part of the suspension and continue to be available to eligible borrowers.

Read also:James Hiroyuki Liao Barry The Visionary Entrepreneur Revolutionizing The Business Landscape

How to Determine If Your Plan Is Affected

To check if your repayment plan is affected, log in to your student loan servicer's website or contact them directly. They can provide detailed information about your specific situation and guide you through any necessary changes.

Why Was the Suspension Implemented?

The Education Department's decision to suspend certain income-driven repayment plans stems from a broader effort to address systemic issues within the student loan repayment system. Key reasons for the suspension include:

- Program Integrity: Concerns about fraudulent claims and misuse of funds.

- Fairness: Ensuring that all borrowers receive equitable treatment under the repayment system.

- Cost Management: Reducing the financial burden on taxpayers while maintaining support for struggling borrowers.

These changes reflect a growing recognition of the need for reform in the student loan sector, particularly as debt levels continue to rise.

Impact on Borrowers

The suspension of certain income-driven repayment plans has significant implications for affected borrowers. Depending on the specifics of their situation, borrowers may experience:

- Increased monthly payments if they are required to switch to a different repayment plan.

- Potential delays in loan forgiveness timelines.

- Increased financial strain due to higher repayment obligations.

However, it's important to note that the Education Department has stated its commitment to supporting borrowers during this transition period. Resources and assistance are available to help individuals navigate the changes.

Support for Affected Borrowers

The Education Department has established a dedicated hotline and online portal to assist borrowers affected by the suspension. These resources provide guidance on available options and steps to take to minimize the impact of the changes.

Steps Borrowers Should Take

While the suspension of certain income-driven repayment plans may seem daunting, there are several steps borrowers can take to protect their financial well-being:

- Review Your Loan Details: Understand the specifics of your current repayment plan and determine if it is affected by the suspension.

- Contact Your Loan Servicer: Reach out to your servicer for personalized guidance and assistance.

- Explore Alternative Options: Consider other repayment plans or consolidation programs that may suit your financial situation.

- Stay Informed: Keep up-to-date with the latest developments and announcements from the Education Department.

Taking proactive steps now can help mitigate the impact of the suspension and ensure a smoother repayment process moving forward.

Prioritizing Financial Health

Managing student loan debt requires careful planning and a commitment to financial responsibility. By staying informed and taking advantage of available resources, borrowers can navigate the challenges posed by the suspension and achieve long-term financial stability.

Exploring Alternative Repayment Options

For borrowers affected by the suspension, exploring alternative repayment options is essential. Some viable alternatives include:

- Revised Pay As You Earn (REPAYE): Offers similar benefits to PAYE but with broader eligibility criteria.

- Income-Contingent Repayment (ICR): Caps payments at 20% of discretionary income and offers loan forgiveness after 25 years.

- Loan Consolidation: Combining multiple loans into a single payment can simplify repayment and potentially lower interest rates.

Each option has its own set of advantages and drawbacks, so it's important to carefully evaluate which one aligns best with your financial goals.

Choosing the Right Plan

When selecting a repayment plan, consider factors such as your current income, expected future earnings, and overall financial situation. Consulting with a financial advisor or student loan counselor can provide valuable insights and help you make an informed decision.

Eligibility Criteria for Remaining Plans

While certain income-driven repayment plans have been suspended, others remain available to eligible borrowers. To qualify for these plans, borrowers must meet specific criteria, including:

- Holding federal student loans.

- Demonstrating financial need based on income and family size.

- Submitting the necessary documentation, such as tax returns and income verification forms.

Eligibility requirements may vary depending on the specific plan, so it's important to review the details carefully before applying.

Verifying Eligibility

To verify your eligibility for a particular repayment plan, use the official Federal Student Aid website or contact your loan servicer. They can provide detailed information about the application process and any required documentation.

Useful Resources for Borrowers

Several resources are available to assist borrowers navigating the changes to income-driven repayment plans:

- Federal Student Aid: Offers comprehensive information on repayment options and eligibility criteria.

- Student Loan Servicers: Provide personalized support and guidance for borrowers.

- Nonprofit Organizations: Organizations like the Student Borrower Protection Center offer advocacy and resources for student loan borrowers.

Taking advantage of these resources can help borrowers make informed decisions and manage their debt effectively.

Building a Support Network

Connecting with other borrowers and joining support groups can provide valuable insights and encouragement during the repayment journey. Sharing experiences and strategies can help individuals feel less isolated and more empowered to tackle their financial challenges.

Future Outlook and Potential Changes

The future of income-driven repayment plans remains uncertain as the Education Department continues to review and reform the system. Potential changes could include:

- Revised eligibility criteria for existing plans.

- Introduction of new repayment options designed to address current shortcomings.

- Increased focus on borrower education and financial literacy programs.

While the exact nature of these changes is yet to be determined, staying informed and engaged with the process is key to ensuring a positive outcome for all borrowers.

Remaining Proactive

As the student loan landscape continues to evolve, borrowers must remain proactive in managing their debt. By staying informed, exploring available options, and seeking support when needed, individuals can navigate the challenges posed by the suspension and achieve financial stability.

Kesimpulan

The Education Department's suspension of certain income-driven repayment plans highlights the ongoing need for reform in the student loan sector. While the changes may present challenges for affected borrowers, there are steps they can take to minimize the impact and protect their financial well-being. By staying informed, exploring alternative options, and leveraging available resources, borrowers can successfully navigate this transition period.

We encourage readers to share their thoughts and experiences in the comments section below. Your input can help others facing similar challenges. Additionally, feel free to explore other articles on our site for more insights into managing student loan debt and achieving financial success.